Corrosion is the slow decay of metallic materials that, over a long period of time, can lead to catastrophic failure of a structure. Investment fees act in a similar nature, slowly and constantly eating away at your returns and severely damaging your potential to buy that house, put your kids through college or retire when you want. The good news is that, like an engineer dealing with corrosion, you can avoid the damage if you make smart decisions to protect yourself.

recent posts

- Achieve Financial Freedom: The Importance of The Number

- Envision Your Financial Future and Plan How to Get There with a Portfolio of Portfolios

- This is Not Your Parents Diversification – Investment STRATEGY Diversification

- Get to Know your Small Business 401(k) Fiduciary…….and Save Millions

- Accelerating Dual Momentum Investing

author

-

-

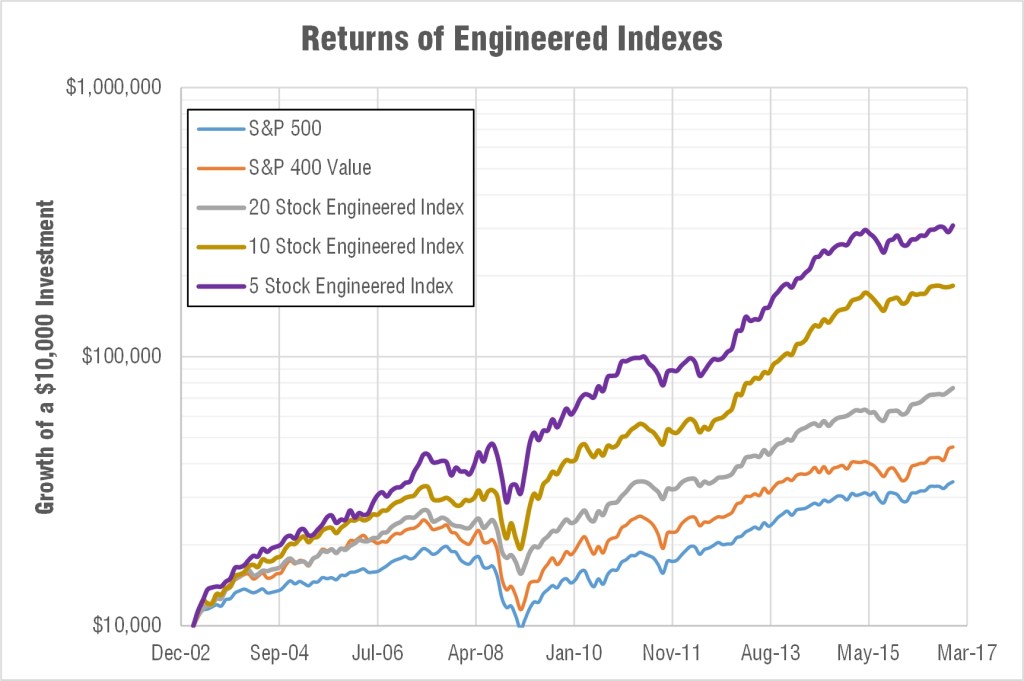

Did our engineered indexes peak your investment interest; but did they still seem a little too risky for what you are comfortable with?

In those indexes we pick US stocks on a monthly basis; and we’ve made an effort to pick stocks across uncorrelated sectors. But at the end of the day, they all still carry US stock market risk. Portfolio management seeks to reduce risk by spreading your investments across many uncorrelated asset classes like international equities, bonds, and gold. So let’s do that with our engineered indexes to engineer a balanced index fund!

In this post we’ll add an allocation to international equities, bonds, and gold to our diversified US equity engineered indexes. What we’ll be left with are two very well diversified funds that have exhibited about half the risk of the S&P 500 while matching, and even beating its returns.

-

Buying an S&P 500 index fund is boring yet simple. In the world of investing, boring and simple generally means inexpensive yet high returns. But if its too boring, excitement seeking humans (like myself) may opt for “sexier” investment opportunities.

The trouble is that sexy stocks and “strategies” are both expensive and their returns are underwhelming. But can we apply some lessons learned from previous analysis to make a boring and simple investment strategy… fun and exciting!?

-

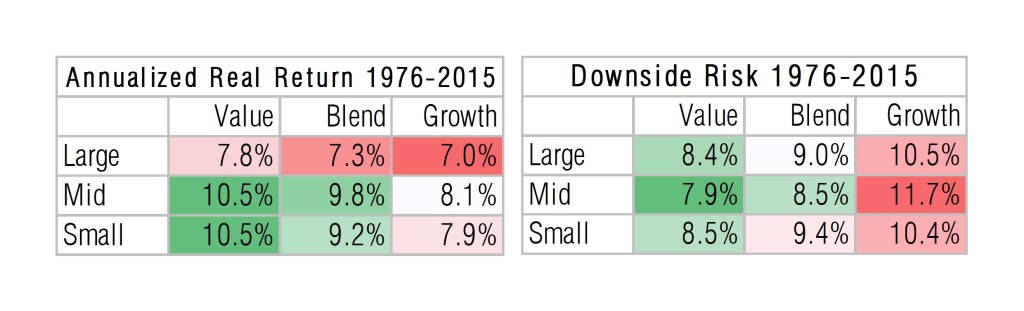

Everyone has heard of the investment adage to “buy low, and sell high.” But it’s very difficult to execute in practice. But the mid-cap value index buys low and sells high automatically for its investor.

In this blog I’ll explain why this area of the equity market is so proficient. But I won’t stop at some simple conjecture, I’ll prove this functionality in other areas of the market. Not only that, we’ll go over a way to capitalize on the mid-cap value’s inherent genius.

-

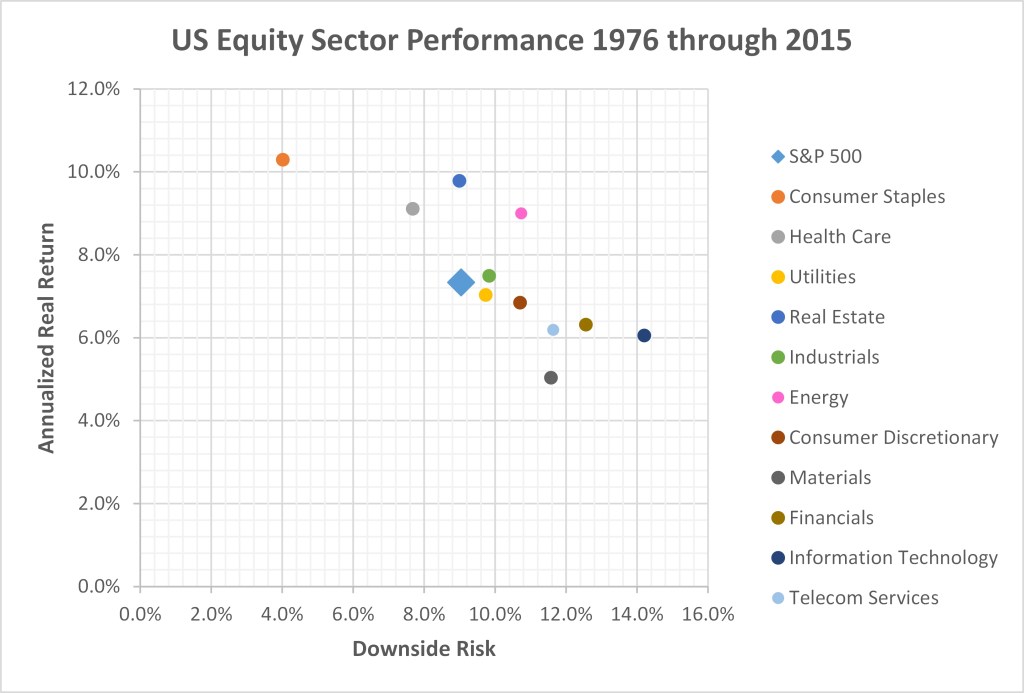

Should stock sectors be created equally? Are there some that consistently outperform and some that consistently underperform?

After my post on the historical performance (and outperformance) of different US stock style boxes I set out to see if a similar phenomena occurs with US stock sectors. Surely the least risky sector won’t also offer the highest performance like what happened with stock style boxes!? Well it does… and in this post we’ll go through the historical data, look at moving trends, calculate some risk metrics, look at the correlation matrix, offer some additional resources and point out some investment opportunities to consider.

-

What area of the market offers the best risk-adjusted returns? Is there a better index to passively invest in and track than the S&P 500?

I’ve always assumed there to be a risk/return relationship between market indexes; but when I began diving a little deeper into the historical data it quickly became apparent that there are certain areas of the market that defy logic and offer higher returns with less risk.

-

In 1952 a guy named Harry Markowitz introduced something known as Modern Portfolio Theory (MPT). Harry won a Nobel prize for his work which mathematically showed how and why risk and return for an individual asset should not be viewed on its own, but on how that asset impacts the overall risk and return of a portfolio of assets. My prior blog post on asset allocation explains the basic mechanics of how different asset classes can impact the risk and return of a portfolio. In this post we will dive a little deeper to show how the efficient frontier is constructed.

-

Stocks are risky but they generate high returns. Bonds are safer but they offer proportionally less returns. Investors may think that combining these asset classes in a portfolio linearly scales risk versus return. For the most part this is true; but due to a lack of correlation between these assets, combining them in a portfolio can actually increase returns without increasing risk.

-

With investing, we all know that if you want to play it safe you buy bonds and that if you want more return and can stomach the risk you buy stocks. But what if I told you that there is a way to have your cake and eat it to, to have less risk AND more return. Normally if you hear this kind of claim from someone I would advise you to run from them and run fast. But in this case I think you should hear me out because engineering a portfolio comprised of the right mix of different asset classes can help you travel on the efficient frontier all the way to the bank.